Imagine being at peace with your finances, knowing your dream home isn’t a budget buster but a smart reality. Capture that feeling, because mastering the 28/36 rule is like having the KonMari method for your mortgage—tidying up your debts and paving the way to financial comfort.

By the end of this post, you’ll have a clear roadmap to manage your housing costs and debt like a pro, ensuring your wallet remains as cozy as your living room.

Quick Takeaways:

- Stick to spending no more than 28% of your gross income on housing to keep living costs in check; it’s your financial guardrail against housing overspend.

- Keep all debt obligations below 36% of your gross income to maintain a buffer zone for savings and investments, lessening the “what if” worries.

- Adjust the 28/36 rule to fit your unique financial situation, allowing for income variations and future goals for a personalized approach to budget mastery.

What Is the 28/36 Rule in Budgeting?

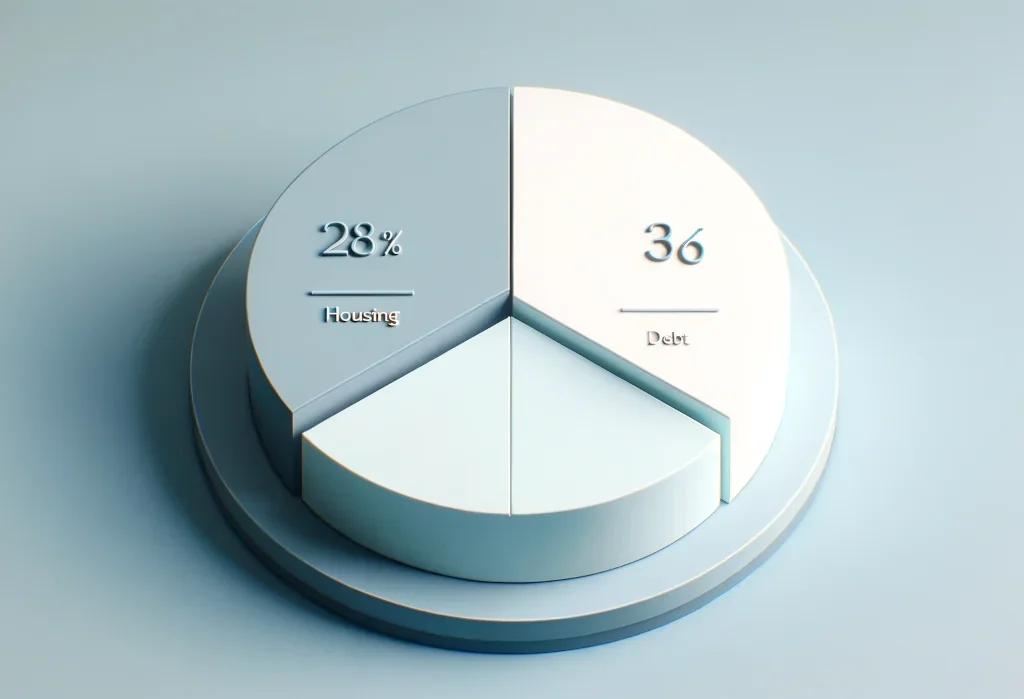

When it comes to managing your money, the 28/36 rule is like an old friend who has got your back. This budgeting guideline helps you figure out just how much of your hard-earned dough should go toward housing costs and keeping those debts at bay.

Here’s the lowdown: Aim to spend no more than 28% of your gross monthly income on housing expenses. This includes mortgage or rent, property taxes, homeowners insurance, and homeowners association fees if you’ve got ’em. And the second part of this friendly advice? Keep your total monthly debt payments — we’re talking housing expenses plus any loans or credit cards — under 36% of your monthly gross income.

Imagine you pull in a cool $5,000 a month before taxes. That means you should ideally keep your housing expenses under $1,400 and your overall debt payments below $1,800. Stick to this, and you’ll be sitting pretty, avoiding most of those sleepless nights stressing about bills.

Why Should You Care About the 28/36 Rule?

So, why cozy up to this 28/36 rule? It’s simple: it’s about protecting your peace of mind and your pocketbook. By sticking to these benchmarks, you can sidestep the trap of living beyond your means — a financial faux pas that can lead to a whole heap of trouble.

The beauty of this rule is it keeps you grounded. It’s like having guardrails on a winding mountain road — it helps prevent you from skidding off into the abyss of debt. Following it could mean you have more cash to save for a rainy day, invest for the future, or even splurge on a much-needed vacation. In other words, it’s your ticket to more financial freedom and less “what if” worry.

How Do You Calculate Your Own 28/36 Ratios?

Calculating your 28/36 ratios doesn’t require a math degree — it’s easier than baking a pie. Grab your latest pay stub, and let’s break it down:

- Determine your gross monthly income: That’s your income before taxes and deductions.

- Calculate 28% for housing: Multiply your gross monthly income by 0.28.

- Calculate 36% for total debt: Multiply your gross monthly income by 0.36.

So, if you’re grossing $60,000 per year, that means your monthly income before taxes is $5,000. Here’s what your budget should look like:

- Housing expenses max: $5,000 x 0.28 = $1,400

- Total debt service max: $5,000 x 0.36 = $1,800

Remember, these figures are the ceiling of your budgeting — not the floor. If you can spend less while still meeting your needs, that’s even better. And here’s a pro tip most folks overlook: the 28/36 rule is just a guideline. Everyone’s financial situation is unique. Maybe you have additional income from a side hustle or you’re planning for a big life change. Adjust the rule to fit your life — because budgeting isn’t one-size-fits-all. It’s all about what works for you.

Here’s a quick snapshot to illustrate how the 28/36 rule pans out across different income levels:

| Income Level | Monthly Income | Max Housing Cost (28%) | Max Total Debt (36%) | Examples of Expenses Within Limits |

|---|---|---|---|---|

| Low Income | $3,000 | $840 | $1,080 | Rent, Utilities, Credit Card Debt |

| Middle Income | $6,000 | $1,680 | $2,160 | Mortgage, Car Loan, Student Loan |

| High Income | $10,000 | $2,800 | $3,600 | Luxury Rent, Personal Loan, Investments |

This table demonstrates the flexibility of the 28/36 rule across various income brackets, showing that financial planning is not about stringent restrictions, but about smart allocation. Notice how the rule scales proportionally, ensuring that even with higher income, financial commitments remain balanced. This approach prevents overextending in debt or housing costs, irrespective of your earnings.

It’s crucial to tailor these numbers to your lifestyle and needs, keeping in mind that less debt and lower housing costs can provide more financial freedom and stability.

Can the 28/36 Rule Work for Everyone?

Let’s face it, folks—a one-size-fits-all approach rarely fits, well, all. The 28/36 Rule is a smart starting point for budgeting, helping many learners keep their finances in check. But does it work for everyone? Well, that’s like asking if everyone can rock skinny jeans—probably not.

Consider Jane, pulling in a cool $50,000 per year with no debt. She’s living comfortably within the 28/36 framework, allocating a reasonable chunk of change toward her housing. Now meet Joe, earning the same but juggling student loans and a car payment. For Joe, this rule might feel like a straitjacket, squeezing out the fun from his budget.

Then there’s Sheila, raking in a hefty six figures. Should she limit herself to the same percentage for housing? Maybe she can afford to splurge on that extra bathroom or a pool in the backyard.

How do you tailor it to your wallet’s contents? Here’s the deal:

- Adjust for Income: If you’re killing it in the income department, maybe you can afford to tilt the scales a bit. It’s your money after all—but don’t get cocky and overcommit.

- Tackle That Debt: For the Joe’s of the world, focusing on debt might mean tweaking the 36% to allow more breathing room.

- Factor in Future Goals: Planning to retire at 50 or start a business? You might want to cinch that belt tighter now.

Remember, it’s about balance—not just blind adherence to numbers.

What Are the Limits and Flexibilities Within the Rule?

The 28/36 Rule isn’t chiseled in stone. It’s more like a guideline drawn in the sand, with room for adjustments.

High-Income Earners : Got cash to burn? The rule can flex for you. If you’re making bank, spending a little extra on a dream home might not shake up your financial stability. But beware—more house often comes with more costs that aren’t always obvious upfront.

High Cost-of-Living Areas : Living in places like San Francisco or NYC might make the 28% for housing seem like a fairy tale. In these cases, stretching that number might be unavoidable, but stretch with caution and know that you might have to compensate elsewhere.

Stretching limits can be tempting, but it’s a bit like juggling fire—it can heat up your life or go up in flames. Understand the risks:

- Higher Stress: Overcommitting financially can turn your Zen den into a house of cards.

- Less Wiggle Room: One slip—a job loss or a major repair—and your budget might do a belly flop.

What Can You Do If Your Ratios Are Off?

If your ratios are looking a little wonky, don’t fret! Here’s the game plan to get back on track:

-

Slash That Debt : Look at paying off high-interest debts first—it’s like giving yourself a raise. Consider tools like the debt snowball or avalanche methods. They’re not just buzzwords; they’re game-changers.

-

Boost Your Income : Side hustle, anyone? Turning a hobby into cash can be easier than you think. Sell your crafts, drive for a rideshare app, or rent out a room.

-

Scrimp and Save : Where can you cut back? Maybe dine out less or swap that fancy gym membership for workouts in the park.

-

Cheaper Housing Options : Consider downsizing or look into more affordable areas if possible. Sometimes, a smaller space can spark more joy than a mega-mansion.

-

Restructure Loans : Can you refinance for a better rate? It might be worth a shot, especially with a sturdy credit score as your wingman.

-

Realistic Budgeting : Switch up your budget to match your real-life spending and saving. Apps like Mint or You Need A Budget can get you sorted.

Here’s a gem most folks miss: Season your budget with a pinch of patience. Quick fixes might seem appealing, but steady, strategic moves build lasting financial health. Don’t just dream about a strong financial future—start laying those bricks today.

By being assertive with your finances, and tackling issues head-on, rather than burying your head in the sand, you’re taking steps toward a future where you’re in control—not your bills. And remember, the goal isn’t just to manage; it’s to thrive. With the right tweaks, these rules and numbers become tools to carve out the life you want, in a home that feels like a castle (even if it’s more of a cozy cottage in size).

Remember, when it comes to financial advice, one size never fits all. Use the 28/36 Rule as your compass, not your cage, and adapt it as your journey unfolds. Your dream home, free from the shackles of overwhelming debt, awaits!

As a financial advisor, my goal is to guide you through the world of personal finance with clear, practical advice. With a dedication to clarity and your financial well-being, I’m here to provide insightful guidance and support as you build a foundation of wealth and security.

")